Fiat

Chrysler Cyber Risk Recall of 1.4M Vehicles Seen as Industry

First

July

26, 2015 by Jeff Plungis and Mark Clothier

Fiat Chrysler Automobiles NV is recalling

about 1.4 million cars and trucks equipped with radios that are vulnerable to

hacking, the first formal safety campaign in response to a cybersecurity

threat.

The move marks a milestone for the

industry, which last year set a record with 64 million autos called back for

fixes in the U.S. The National Highway Traffic Safety Administration, under fire

from Congress for not catching defects more quickly, has been considering

punitive action against Fiat Chrysler for failing to protect vehicle

owners.

Unauthorized remote access to certain

vehicle systems was blocked with a network-level improvement on July 23, the

company said in a statement. In addition, affected customers will receive a USB

device to upgrade vehicles’ software with internal safety

features.

Fiat Chrysler was already distributing

software to insulate some connected vehicles from illegal remote manipulation

after Wired magazine published a story about software

programmers who were able to take over a Jeep Cherokee being driven on a

Missouri highway.

The company, led by Chief Executive

Officer Sergio Marchionne, reiterated that it’s not aware of any real-world

unauthorized remote hack into any of its vehicles. It stressed that no defect

was found and said it’s conducting the campaign out of “an abundance of

caution.”

NHTSA said it encouraged the action to

protect consumers against a vulnerability that could affect a driver’s

control.

Expanded

Action

“Launching a recall is the right step to

protect Fiat Chrysler’s customers, and it sets an important precedent for how

NHTSA and the industry will respond to cybersecurity vulnerabilities,” NHTSA

Administrator Mark Rosekind said in a statement Friday.

The recall covers about a million more

cars and trucks than those initially identified as needing a software patch. The

action includes 2015 versions of Ram pickups, Jeep Cherokee and Grand Cherokee

SUVs, Dodge Challenger sports coupes and Viper supercars.

“That’s not a small number to go after,”

Mark Boyadjis, an analyst with IHS Automotive, said in a telephone interview.

“This is a pretty quick response and much of it could be P.R. driven. But I

think it will keep consumers comfortable and prevent current ones and future

ones from straying away from the brand.”

This isn’t the first time automobiles

have been shown to be vulnerable to hacking. What elevates this instance is that

researchers were able to find and disable vehicles from miles away over the

cellular network that connects to the vehicles’ entertainment and navigation

systems.

That capability makes the possibility of

remote hacking of cars a reality. Earlier hacks have mostly been achieved by

jacking the researchers’ laptops into diagnostic ports inside the

cars.

Fiat Chrysler’s UConnect infotainment

system uses Sprint Corp.’s wireless network.

“This is not a Sprint issue but we have

been working with Chrysler to help them further secure their vehicles,” said

Stephanie Vinge Walsh, a Sprint spokeswoman.

NHTSA said it would open an investigation

of the remedy “to ensure that the scope of the recall is correct and that the

remedy will be effective,” agency spokesman Gordon Trowbridge said in an

e-mailed statement. The agency said its electronics and cybersecurity experts

will continue to monitor hacking threats and take action when

necessary.

Consumer

Confidence

There’s a possibility the recall could

affect consumer confidence in Fiat Chrysler, even though the company isn’t the

only one with cybersecurity challenges, said Thilo Koslowski, vice president and

automotive practice leader at technology consultant Gartner

Inc.

“It validates that cyber-hacking with

cars is a serious issue that the auto industry must pay attention to,” he said.

“The auto industry needs to develop new technology to combat these technological

problems.”

General Motors Co. has a team working on

cybersecurity and has hired Harris Corp.’s Exelis and other firms to develop

anti- hacking systems, said Mark Reuss, the Detroit automaker’s executive vice

president for global product development. GM seeks to block hackers’ access to

its autos, he said, and if they do get in, it tries to prevent them from gaining

control.

“It’s probably one of the most important

things we spend time on,” Reuss said. “Anyone who wants to do something like

that will probably get on, so you have to look at what happens when they

do.”

Proposed

Legislation

GM has also worked with the U.S. military

and with Boeing Co. on its anti-hacking systems, he said.

Senators Edward Markey of Massachusetts

and Richard Blumenthal of Connecticut, both Democrats, introduced legislation on

July 21 that would direct NHTSA and the Federal Trade Commission to establish

rules to secure cars and protect consumer privacy.

The senators’ bill would also establish a

rating system to inform owners about how secure their vehicles are beyond any

minimum federal requirements. The lawmakers released a report in 2014 on gaps in

car-security systems, concluding that only two of 16 automakers had the ability

to detect and respond to a hacking attack.

Markey questioned why it took nine months

after learning about the security gap for Fiat Chrysler to order a

recall.

‘No

Assurances’

“There are no assurances that these

vehicles are the only ones that are this unprotected from cyberattack,” he said

Friday in an e-mail. “A safe and fully equipped vehicle should be one that is

equipped to protect drivers from hackers and thieves.”

Although general cyber threats have been

acknowledged previously by the industry, the specific ability to take control of

critical vehicle functions in the affected Fiat Chrysler vehicles only became

clear with the Wired magazine

report, said Fiat Chrysler spokesman Eric Mayne.

“Prior to this month, the precise means

of the demonstrated manipulation was not known,” Mayne

said.

Representatives Fred Upton and Frank

Pallone, leaders of the House Energy and Commerce Committee, sent letters to 17

manufacturers and NHTSA in May to gather information about how the industry is

addressing cybersecurity.

“As the underlying technologies seemingly

evolve by the day, so too must our manufacturers and regulators keep pace to

protect drivers from these growing threats,” the Michigan Republican and New

Jersey Democrat said in a statement Friday.

(By Bloomberg Reporters Mark Clothier and

Jeff Plungis; with assistance from Patrick Ralph in New York, David Welch in

Southfield, Michigan, and Jordan Robertson in Washington.)

Copyright 2015

Bloomberg.

Hackers Remotely Kill a Jeep on the Highway—With Me in It

Though I hadn’t touched the dashboard, the vents in the Jeep Cherokee started blasting cold air at the maximum setting, chilling the sweat on my back through the in-seat climate control system. Next the radio switched to the local hip hop station and began blaring Skee-lo at full volume. I spun the control knob left and hit the power button, to no avail. Then the windshield wipers turned on, and wiper fluid blurred the glass.

As I tried to cope with all this, a picture of the two hackers performing these stunts appeared on the car’s digital display: Charlie Miller and Chris Valasek, wearing their trademark track suits. A nice touch, I thought.

The Jeep’s strange behavior wasn’t entirely unexpected. I’d come to St. Louis to be Miller and Valasek’s digital crash-test dummy, a willing subject on whom they could test the car-hacking research they’d been doing over the past year. The result of their work was a hacking technique—what the security industry calls a zero-day exploit—that can target Jeep Cherokees and give the attacker wireless control, via the Internet, to any of thousands of vehicles. Their code is an automaker’s nightmare: software that lets hackers send commands through the Jeep’s entertainment system to its dashboard functions, steering, brakes, and transmission, all from a laptop that may be across the country.

To better simulate the experience of driving a vehicle while it’s being hijacked by an invisible, virtual force, Miller and Valasek refused to tell me ahead of time what kinds of attacks they planned to launch from Miller’s laptop in his house 10 miles west. Instead, they merely assured me that they wouldn’t do anything life-threatening. Then they told me to drive the Jeep onto the highway. “Remember, Andy,” Miller had said through my iPhone’s speaker just before I pulled onto the Interstate 64 on-ramp, “no matter what happens, don’t panic.”1

Immediately my accelerator stopped working. As I frantically pressed the pedal and watched the RPMs climb, the Jeep lost half its speed, then slowed to a crawl. This occurred just as I reached a long overpass, with no shoulder to offer an escape. The experiment had ceased to be fun.

At that point, the interstate began to slope upward, so the Jeep lost more momentum and barely crept forward. Cars lined up behind my bumper before passing me, honking. I could see an 18-wheeler approaching in my rearview mirror. I hoped its driver saw me, too, and could tell I was paralyzed on the highway.

“You’re doomed!” Valasek shouted, but I couldn’t make out his heckling over the blast of the radio, now pumping Kanye West. The semi loomed in the mirror, bearing down on my immobilized Jeep.

I followed Miller’s advice: I didn’t panic. I did, however, drop any semblance of bravery, grab my iPhone with a clammy fist, and beg the hackers to make it stop.

For the rest of this article, please visit: http://www.wired.com/2015/07/hackers-remotely-kill-jeep-highway/

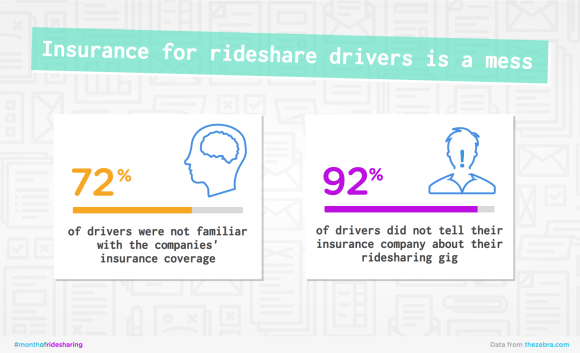

Josh Waldrum knows from firsthand experience that most of the folks who drive for rideshare services like Uber and Lyft are not well informed about the insurance issues that insurance professionals see as problematic, such as coverage gaps and the amounts and types of coverage needed.

Josh Waldrum knows from firsthand experience that most of the folks who drive for rideshare services like Uber and Lyft are not well informed about the insurance issues that insurance professionals see as problematic, such as coverage gaps and the amounts and types of coverage needed.